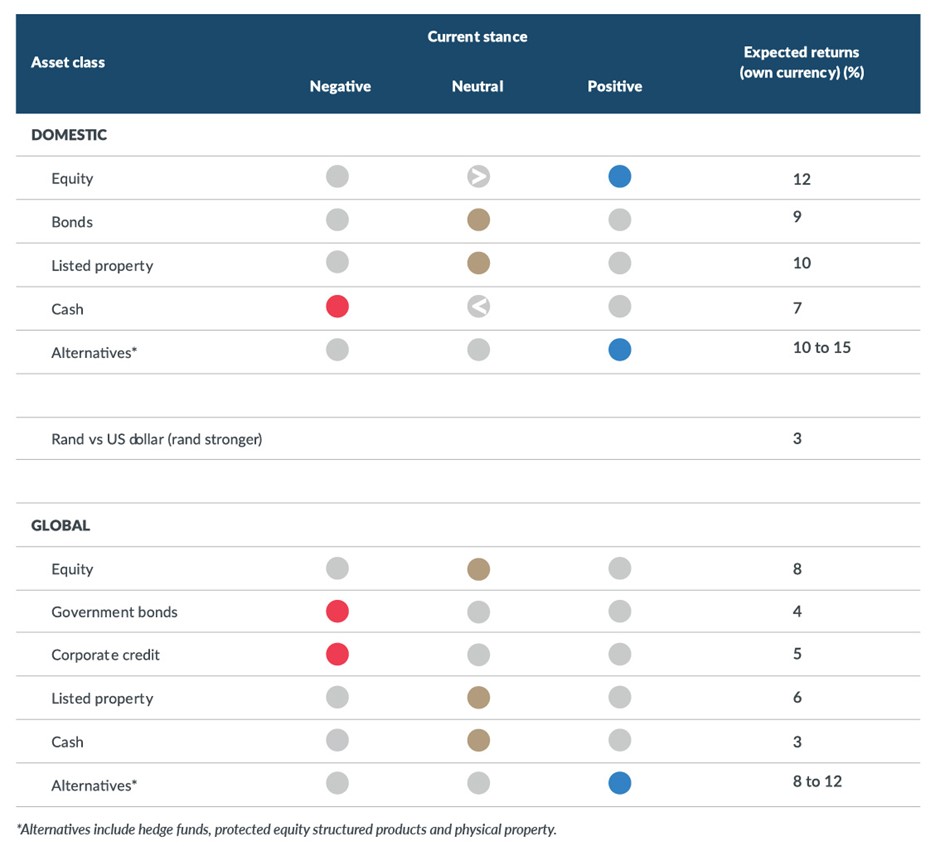

Anchor Capital asset allocation, 1Q26

Since the publication of The Navigator – Anchor’s Strategy and Asset Allocation, 4Q25 in October 2025, we have implemented only two changes to our domestic asset allocation framework, while maintaining our existing positioning across global asset classes. Our overarching stance remains constructive, underpinned by resilient earnings growth, moderating inflation dynamics and an improving monetary policy backdrop.

Domestic positioning

Within South African asset classes, we have upgraded our view on JSE-listed equities from neutral to positive. This adjustment reflects improving earnings momentum, supportive commodity prices and valuations that remain reasonable relative to global peers. Conversely, we have downgraded our neutral stance on domestic cash from neutral to negative as declining interest rates reduce its attractiveness. We maintain a neutral stance on domestic bonds and JSE-listed property.

Global positioning

From a global perspective, our views are unchanged. We continue to hold neutral positions in global equities, listed property, and cash, while maintaining a more cautious negative stance on global government bonds and corporate credit. Overall, we remain constructively positioned toward risk assets within a diversified framework, supported by disciplined capital allocation and a long-term investment horizon.

Market backdrop

The constructive momentum propelling global markets is expected to persist. While valuations remain elevated and volatility is likely to remain above long-term averages, it is our assessment that underlying earnings growth will remain robust and continue to support risk assets. Sectors exposed to artificial intelligence (AI)-driven capital expenditure continue to demonstrate strong revenue trajectories, reinforcing the broader market performance. We also expect the US interest rate-cutting cycle to continue, which will provide further impetus to investors’ risk appetite and support asset prices. While monetary policy remains data dependent, the broader direction appears favourable for diversified portfolios with measured risk exposure.

The role of alternatives

Within this environment, we maintain a favourable view on alternative assets, including hedge funds, protected equity structured products, physical property, etc., both domestically and abroad. These asset classes offer attractive risk-adjusted return profiles and exhibited more defensive characteristics during periods of heightened volatility. Although alternatives remain underrepresented in most South African portfolios, they command a significant share of the investment wallet for family offices abroad. We expect most domestic investors will benefit by gradually increasing their exposure to this asset class over time, particularly as declining interest rates enhance their attractiveness.

Offshore allocation and currency considerations

Anchor is a proponent of balanced portfolios and diversified risks. We maintain that it is crucial for investors to have a long-term plan for what they seek to achieve with their investments, and we think that the year ahead will likely see them move towards their eventual desired outcome. In our view, this is an excellent time to take a pro-risk stance in your portfolio. We advocate that a healthy portion of your investment portfolio should be offshore to leverage diverse opportunities and return profiles while mitigating SA-specific risk. At current levels, we view the rand exchange rate as reasonably valued against the US dollar, providing an appropriate opportunity to externalise a portion of your portfolio. Although we expect the rand to hover around these levels over time, we also find that the investment opportunities abroad are compelling.

Expected returns

Figure 1: Anchor Capital expected returns by asset class, domestic and offshore (Source: Anchor Capital)

While return expectations across asset classes remain constructive, we find global equities particularly compelling given earnings resilience and structural growth drivers. Domestically, we anticipate continued support for equities, aided by commodity strength and improving investor sentiment.